According to a recent survey conducted by Closing Corp, over half of all home buyers are surprised by the closing costs required to obtain their mortgage.

After surveying 1,000 first-time and repeat home buyers, the results revealed that 17% of home buyers were surprised that closing costs were required at all, while another 35% were stunned by how much higher the fees were than expected.

“Home buyers reported being most surprised by mortgage insurance, followed by bank fees and points, taxes, title insurance and appraisal fees.”

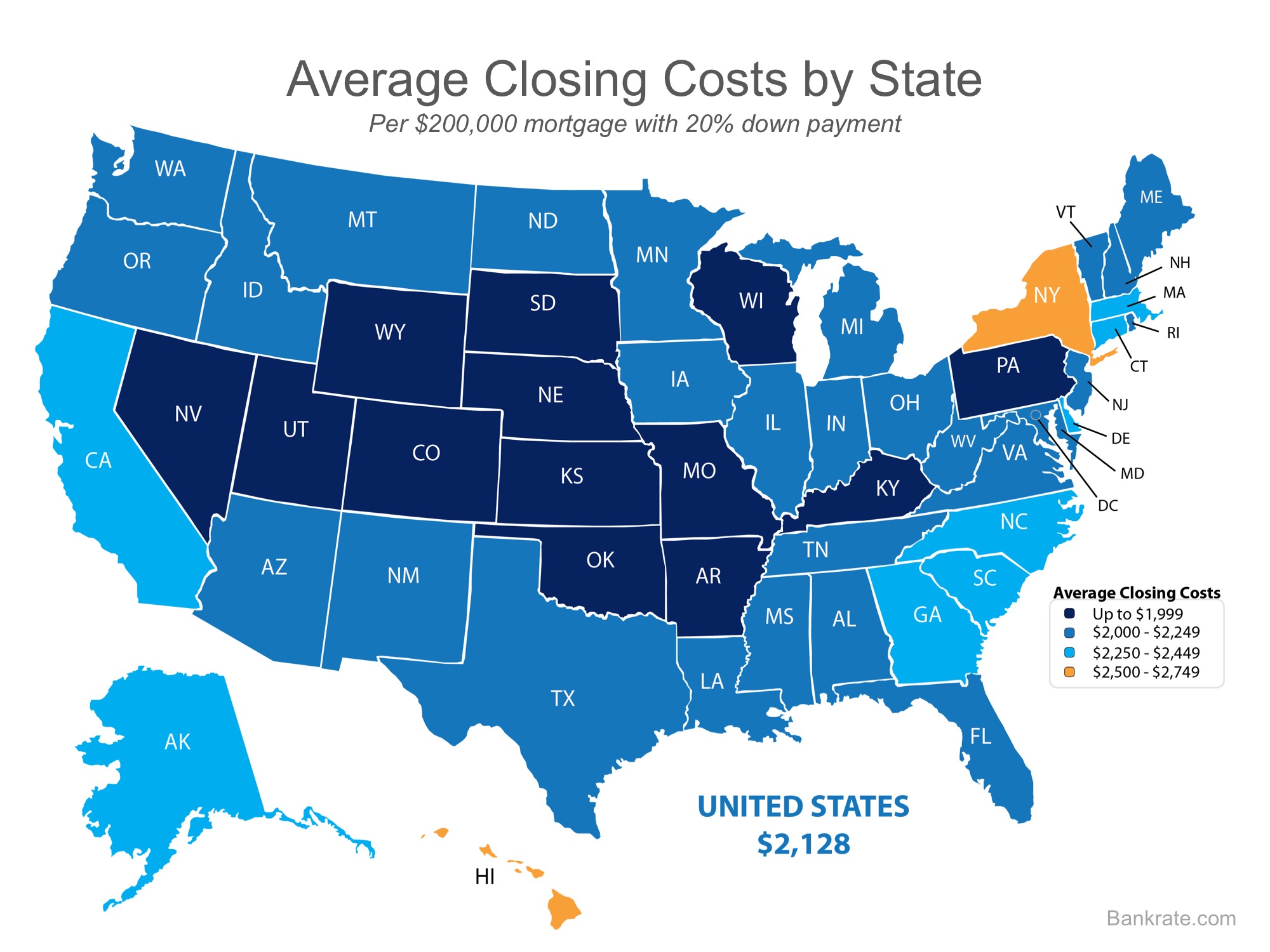

Bankrate.com recently gathered closing cost data from lenders in every state and Washington, D.C. to be able to share the average costs in each state. The map below was created using the closing costs on a $200,000 mortgage with a 20% down payment.

Keep in mind that if you are in the market for a home above this price range. your costs could be significantly more. According to Freddie Mac,

“Closing costs are typically between 2 and 5% of your purchase price.”

Bottom Line

Speak with your lender and agent early and often to determine how much you’ll be responsible for at closing. Finding out that you’ll need to come up with thousands of dollars right before closing is not a surprise anyone is ever looking forward to.

[…] complete the real estate transaction. These costs are in addition to the price of the home and are paid at closing. They include points, taxes, title insurance, financing costs, items that must be prepaid or […]